Grid battery storage is often proposed as the quick fix for variable renewables, but many projects stall long before the first cell arrives. The main keyword appears here: grid battery storage. This article condenses where delays and costs actually come from in 2026, and what practical choices shorten the wait. Readers will learn which technical, regulatory and financial bottlenecks matter most and which policy or market moves tend to clear them fastest.

Introduction

When a transmission operator, a municipality or a factory plans a large battery, the promise is simple: store renewable power when it is abundant and release it when needed. In practice, developers face a chain of steps—permitting, grid studies, hardware procurement, financing and local acceptance. Each step can add months or years. The result in many European countries is long connection queues, stalled projects and cost increases that undermine otherwise sound economics.

This article follows the route from an initial project idea to commercial operation and highlights the concrete frictions that are most likely to create multi‑year delays. Using public reports and recent industry analysis, it explains why some delays are bureaucratic, some are physical (transformers, civil works) and some are market‑design problems (how storage is priced and balanced). The aim is to give a clear picture for readers who want to understand why adding capacity is harder than it looks—and what practical changes shorten the path to operation.

Grid battery storage fundamentals

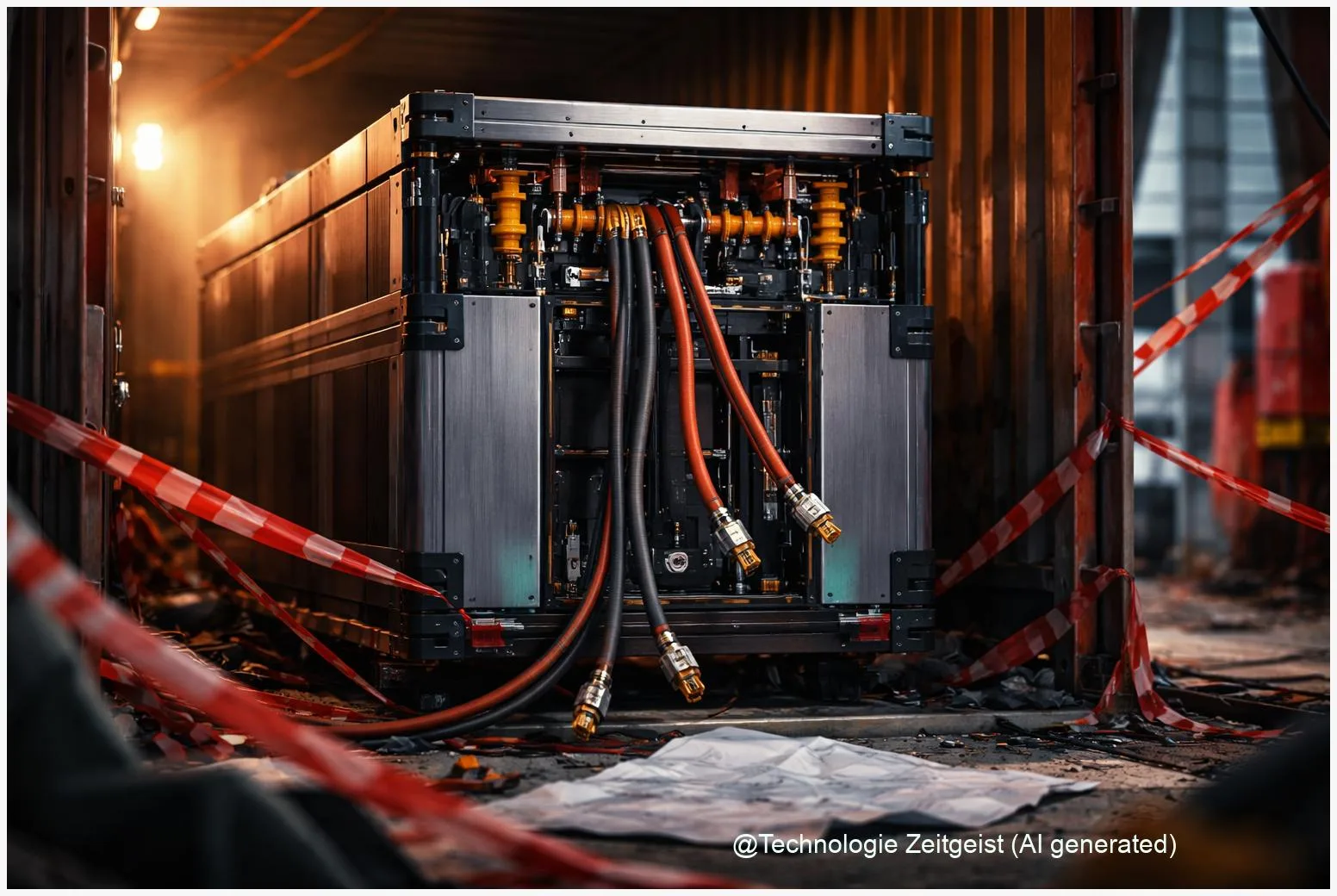

A large grid battery is an engineered system: cells and modules, a battery management system (BMS), an inverter (which converts DC to AC), transformers and often a container or building plus cooling and fire‑safety systems. For planners the two essential measures are power (MW) and energy (MWh). Power determines how much the system can deliver at once; energy determines how long it can sustain that output. Typical utility‑scale systems quoted in industry reports range from a few MW / a few MWh up to several hundred MW with multiple hours of storage.

Two practical constraints matter for the rest of the story. First, physical grid capacity at the chosen substation—transformer capacity, overhead or underground cable rating and short‑circuit levels—must be available or reinforced. Second, regulatory and market treatment defines how the battery earns money: if rules double‑charge storage for both charging and discharging or if accounting and balancing rules are unclear, the business case weakens.

Access to a nearby transformer and a clear connection path are as decisive as the battery technology itself.

A short table helps compare the main categories of bottlenecks and their typical effect on project lead time.

| Bottleneck | What it affects | Typical delay |

|---|---|---|

| Queue for grid connection | Time‑to‑connect; developer certainty | 6–36 months or more |

| Permitting / local approvals | Construction start | 6–24 months |

| Transformer / cable hardware | Physical feasibility | 6–18 months |

These numbers are broad ranges and depend on the country and grid operator. Still, they show why planners often say the battery itself is the easiest part: cells can be delivered in months if financed, while the network and permitting steps are where time accumulates.

Practical bottlenecks on the ground

The most visible bottleneck across Europe in 2025–2026 has been connection queues. Several national TSOs and DSOs reported multi‑GW pipelines of connection requests, many of which cannot be processed quickly because network studies are sequential and resource‑intensive. Analysts have described these lists as containing a significant share of inactive or speculative entries—so‑called “zombie” projects—that occupy capacity without near‑term intent to build.

A second cluster of issues is the sequencing and duplication of studies. Developers typically need a feasibility study, a full grid impact study and then detailed design approvals. If each stage is handled separately by different teams or in a strict serial order, the total latency grows. Consultancies and TSOs have proposed regional “batch” studies that evaluate several projects together to reduce iteration and time.

Third, the hardware chain matters. High‑capacity transformers and high‑voltage cables are specialized items with long lead times. During 2022–2025 global supply‑chain bottlenecks and factory ramps changed lead‑time expectations. In some EU markets the constraint is not cells but transformers, civil works and skilled crews. Public finance instruments that support critical path components—transformers or grid reinforcement—can therefore speed many projects.

Finally, regulatory treatment of storage influences deployment tempo. Variations in metering rules, double‑charging of network fees for charging and discharging, or lack of clear market products for batteries reduce bankability. Recent position papers and reports from grid associations and consultancies recommend harmonized accounting rules and hosting‑capacity maps from DSOs to reduce risk for siting and financing.

For a concrete national example, Spain’s late‑2025 funding round aimed to accelerate 9.4 GWh of storage by tying finance to milestones—but that funding still faces the same connection and permitting hurdles described here (see the project list announced by national agencies for details). A practical link to one such announcement is the TechZeitGeist report on the Spanish programme.

Readers who follow industrial reuse of batteries should also note that second‑life EV packs are being piloted for factory peak‑shaving; these projects face similar grid and permitting requirements even if their cell costs are lower. For background on reuse pilots, see TechZeitGeist’s coverage of automakers reusing EV batteries for factories.

How bottlenecks slow actual projects

Delays are not only inconvenient; they break financial models. Developers plan revenue streams across power markets, balancing services and capacity payments. If connection is postponed by a year, expected returns shrink and some projects lose investor support. In practice, financing agreements often include time‑sensitive clauses: subsidies that require commissioning within a defined window, or loans tied to expected project cashflows. Missing a milestone can mean losing grant money or paying higher financing costs.

Another real effect is site selection bias. Because grid hosting capacity and time‑to‑connect vary regionally, developers tend to cluster where the connection path is faster. That helps some local grids but leaves other regions under‑served and can increase overall curtailment of renewable energy. A lack of transparent hosting maps from DSOs makes it harder for planners to choose sites that balance cost and speed.

Operational risk also increases with waiting time. Components secured early may face obsolescence or price decline; conversely, waiting for the last equipment to align with grid readiness can lead to contractor idle time. Projects that stretch over many years also face political and regulatory changes, which introduces additional risk for long‑lived assets.

Finally, the cumulative system cost rises. When storage cannot come online, grid operators rely longer on fossil‑fueled reserves, curtail renewable output in congested regions, and postpone EV integration benefits. Independent analyses and system operators’ outlooks quantify this as higher overall system costs and slower reductions in curtailment and emissions when storage rollout lags.

Policy and market levers to unblock capacity

Several practical levers cut through the main bottlenecks. First, queue hygiene: introduce binding milestones and “use‑it‑or‑lose‑it” rules so inactive reservations are removed and capacity reallocates to ready projects. Pilots combining milestone mandates with graduated fees have reduced backlog growth in some test regions.

Second, batch network studies and digital tools. Running regional rather than project‑by‑project impact assessments reduces iterative checks. Digital modelling and automated study templates (sometimes using digital twins) speed assessments and clarify network headroom for developers and investors.

Third, flexible connection offers. Time‑limited or interruptible connections allow projects to start earlier at lower capital cost and accept temporary operational constraints until full reinforcements are built. Such arrangements must come with clear compensation rules for curtailment and a path to firm access.

Fourth, targeted finance for critical hardware. Public‑private blended finance can de‑risk procurement of long‑lead items like transformers and cabling or co‑finance distribution reinforcements in high‑value zones. This approach reduces one of the most predictable schedule risks.

Lastly, harmonized market rules for storage—clear measurement and settlement rules, removal of double net‑charges and access to multiple value streams—make business cases resilient to modest delays. Regulators and TSOs that publish hosting maps and standardized metrics also reduce information asymmetry and speed developer decisions.

Where reforms have been piloted, time‑to‑connect medians fell noticeably. The combination that works fastest in practice is transparent data (hosting maps), queue‑discipline and targeted capital support for grid hardware.

Conclusion

Large‑scale batteries will be central to a cleaner grid, but the limiting factors in 2026 are rarely the battery chemistry itself. Most delays and cost increases stem from queue management, sequential network studies, limited availability of transformers and cables, and inconsistent regulatory treatments that make storage harder to finance. Addressing these issues is largely a systems problem: better data from DSOs, binding milestone regimes, batch studies and targeted finance for critical hardware shorten the path to operation. Where these measures are combined, projects move faster and deliver the flexibility the system needs.

If you are following a local storage project, focus early on the connection pathway, ask for hosting‑capacity information, and build contractual flexibility for equipment lead times. Those practical steps matter as much as choosing the battery technology.

Share your experience with grid storage projects and what authorities should prioritise when granting connections.

Leave a Reply